As storms approach, how do we reduce the risk of damage? How might we protect the ones we love, the places we value and the environment that sustains us?

Let’s continue our trek to COP29, the “Finance COP,” in Baku, Azerbaijan, by learning how to “de-risk” as the storm advances.

The United States Environmental Protection Agency associates rising global average temperatures with weather pattern changes leading to:

- Elevated U.S. and Global Temperatures

- More Frequent and Longer Heat Waves

- Changes in U.S. and Global Precipitation

- Increased, Abnormally High Precipitation

- Regional River Flooding

- More Severe Drought in the Southwest

The June 27, 2024 Climate Innovation Forum examined potential responses to such risks. One session, entitled “De-Risking the Transition,” featured Rowan Douglas, Chief Executive Officer of Climate Risk and Resilience for Howden, a specialist insurance broker with an international reach and perspective.

Insurance? Can insurance really make a difference in our response to environmental challenges? According to Rowan Douglas: “Yes!” We can “de-risk.”

(Howden Climate Parametrics, has (re)insurance, climate and data expertise to facilitate risk transfers “across industries, financial markets and the public sector.”)

De-risking, a concept from the financial world, has become increasingly important in an environmental context. It means using financial tools to spread the risks associated with, for example, funding a climate-smart project in a developing country.

The World Resources Institute (WRI), established in 1982 with funding from the MacArthur Foundation, has a guide to de-risking mechanisms to support infrastructure needs in emerging markets and developing nations.

WRI notes that potential funders may perceive the risks to be:

Political – The developing country might have an unstable political environment or experience shifting policy priorities under new leadership.

Regulatory – The nation may have inadequate or contradictory policies, weak legal and enforcement capacity or frequent regulatory changes.

Market – The country might have fragmented or inefficient financial markets and be subject to frequent currency fluctuations.

Technological – The developing country may have limited expertise to realize the proposed project and the required supporting infrastructures may be lacking.

Given these perceived risks, how might an otherwise unbankable project attract institutional and commercial investors to encourage the flow of capital where it is needed?

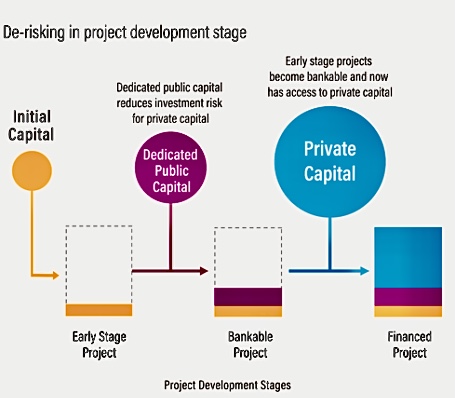

“Typically, this involves public entities such as donor governments, multilateral development banks, development financial institutions and climate funds encouraging private investors to deploy capital by offering to bear a share of the risk. De-risking can be achieved through a range of measures such as debt, equity and guarantees spreading the risk among participating parties or transferring the risk to a third party.” (For a deeper dive into these tools).

Here is an illustration of how “de-risking” might occur:

(A flow chart prepared by the World Resources Institute)

Rowan Douglas observed during the June 27th Forum, that insurance had been in the lower echelon of the financial class system. But the financial world had reached a turning point due to climate change.

“I think we have reached a turning point, because people are now waking up to insurance and insurability as probably being the canary in the cage for valuation risk of physical assets. And they are waking up to the fact that without insurance you can’t get access to credit and can’t get access to capital. So suddenly, it’s becoming a more strategic issue.” (Forum).

He sees insurance as a “mechanism,” a means for finance and public policy to collaborate to create a reasoned response to climate risk. He harkened back to historic examples of de-risking in response to 19th century challenges.

(Image from: My Journal Courrier. The 19th century urban conflagrations in the United States resulted in limited insurance coverage and reduced access to credit and capital. This was the catalyst for public policy changes leading to refined fire codes)

(Image from the Univ. of Cambridge. Mr. Douglas noted that the 19th Industrial Revolution in the United Kingdom caused families to be “wrenched from their rural roots,” into “massive urbanization” and “precarious jobs in factories.” The societal response was a “social insurance revolution.”)

So in our current century, as we address storms caused by climate change, how might we de-risk society to achieve a just transition to a carbon free environment?

Rowan Douglas proffered the June 23, 2024 report, published by Boston Capital Group (BCG), “New Measures of Success for Climate Adaptation and Resilience” and the first de-risking summit.

(Image from Boston Consulting Group)

The key point of the BCG report and summit is that a new approach to de-risking is needed to, in this instance, support climate-smart projects for adaptation to climate change and environmental resilience. Tracking the impact of a country’s natural disaster risk and climate risk could unlock investment to de-risk by:

- Helping public and private investors to identify high-impact projects

- Assisting governments and donors to attract private-sector capital and direct it toward impactful solutions

- Supporting climate-standard-setting bodies in developing a universal adaptation and resilience measurement framework

“Climate risk disclosure is making the risk explicit, which means it needs to be de-risked and in a number of countries – Italy is the latest example – governments are saying to … businesses you’ve got to have insurance risk against natural disaster risk and climate risk, because [governments] are tired of picking up the tab.” (Forum).

One potential outcome is that this will drive the search for modifications to the societal behavior causing climate change, stem the resulting damage to the environment and enable flows of much needed financing to lower and middle income countries.

“[The] thing about insurance is it’s actually the intellectual spine for making lots of difficult decisions. We take insurance for granted as an industry, but it’s … an institution of societies blending science, culture, philosophy … and mathematics that … can give us a rational view of a future and future choices.” (Forum).

In closing, Rowan Douglas offered a hopeful story about Roma, a city in Queensland, Australia, where climate-related natural disasters were such a risk that insurance became hard to secure, capital flows for investment were impeded and people had difficulty obtaining credit to live in Roma.

“The city created the standards for actually defending the city from – in this case – floods and the city became insurable, became investable. So my contention is that what we need are governments, policy, insurers and investment and capital to come together in harmony both in the short term and the longer term to work through as we did in the 19th century.”

Let’s remember this story as we resume our travel together to COP29, the “Finance COP,” in Baku, Azerbaijan.

Guest Blog: Swimming in East Jerusalem by Amy Quirk

Guest Blog: Swimming in East Jerusalem by Amy Quirk